A checklist for home buyer planner is a useful tool to methodically assess different properties during a house hunt by retaining information such as room conditions, exterior condition, and systems in a property. It is an equally good tool for a novice buyer preparing to face the real estate arena for the very first time or a seasoned investor comparing several different properties. A home buyer planner checklist is also available online at Planwiz and includes sections for providing information on different properties, condition ratings, systems ratings, and kitchen quality ratings.

House hunting may become overwhelming, especially when visiting several homes in short periods, which may result in one forgetting some information, especially where some homes have similar features. The house hunting checklist planning tool will help you do that, as it’s available in a PDF format that one can print as well as a digital version that one can edit.

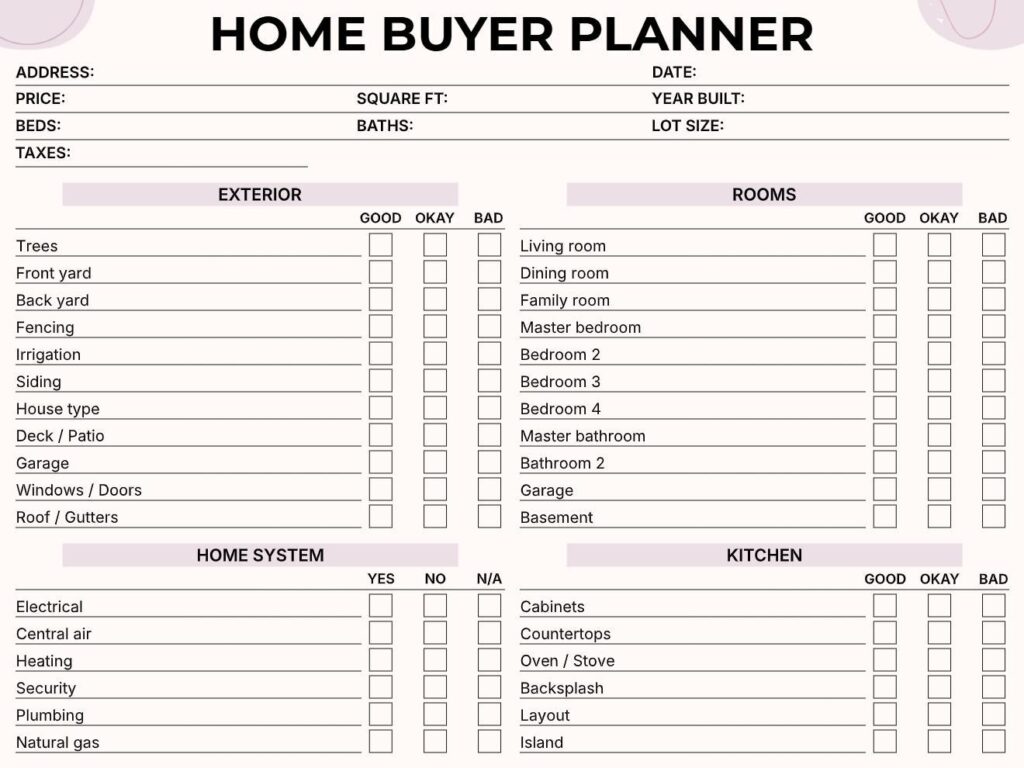

What is a Checklist for Home Buyer Planner?

A checklist for home buyer planner refers to an organized checklist or plan for home buyers to facilitate effective evaluation and comparison of various homes as part of the house hunting process. The checklist typically takes the form of a standardized plan consisting of different home-related categories such as information acquired, home exterior condition, home interior rooms, home systems, and kitchen areas, which require evaluation or comparison. In contrast, the home buyer makes use of a rating method such as good/okay/bad or yes/no/n/a to rate various elements in the home.

This tool will provide a handy memory aid as you view properties and a comparison tool later when reviewing the various homes you have seen. The checklists that you prepare will allow you to make a comparison of all properties that you have looked at in relation to each other and hence help you better to find out which one is best value. This will allow confident decisions to be made without any emotional responses or memories.

What Should Be in Checklist for Home Buyer Planner When Viewing Properties?

If you’re on the path of buying your very own home, as a first-time homebuyer, navigating the viewings of the home can be quite overwhelming, to begin with. With the following checklist, the key areas as a first-time homebuyer to make the most of your dream purchase can be simplified.

Structural Red Flags

| What to Check | Warning Signs | Why It Matters |

|---|---|---|

| Foundation | Cracks wider than ¼ inch, uneven floors, doors that won’t close | Repairs: $10,000–$50,000+ |

| Walls & Ceilings | Large cracks, water stains, soft spots | Indicates foundation movement or leaks |

| Windows & Doors | Gaps, difficulty opening, condensation between panes | Poor insulation = high energy bills |

Major Systems Age Check

Ask the seller these critical questions:

Roof: How old is it? (Replace at 20-25 years = $8,000-$15,000)

HVAC: When was it last serviced? (Lifespan: 15-20 years = $5,000-$10,000)

Water Heater: What year was it installed? (Lifespan: 8-12 years = $1,200-$2,500)

Electrical Panel: What’s the amperage? (Need 200-amp for modern homes)

Water Damage Detection

✅ Test every faucet – Check water pressure and drainage speed

✅ Look up – Ceiling stains indicate roof or plumbing leaks

✅ Look down – Soft floors near bathrooms/kitchen signal hidden leaks

✅ Smell test – Musty odors in basement mean moisture problems

Neighborhood Checklist

Beyond the house itself, evaluate:

- Visit at different times: weekday morning, weekend evening

- Check school ratings (affects resale value even without kids)

- Google “[address] crime statistics”

- Drive your work commute during rush hour

- Knock on a neighbor’s door and ask about the area

Before You Make an Offer

- Get mortgage pre-approval (not just pre-qualification)

- Budget 2-5% of purchase price for closing costs

- Research 3-5 comparable home sales in the neighborhood

- Plan for professional inspection ($400-$600)

- Calculate total monthly costs: mortgage + taxes + insurance + HOA + utilities

- Create to do planner templates for post-offer tasks like scheduling inspections, finalizing mortgage paperwork, and coordinating moving logistics

First-time buyer mistake: Maxing out your budget. Leaving room for future furniture, repairs, and unexpected expenses. Being clear on your goals as a homeowner, a goal planner helps to clarify the needs versus the nice factors while house hunting.

How Much House Can I Afford? Calculate Your Real Budget in 4 Steps

Before you start using your checklist for home buyer planner to evaluate properties, determine your realistic budget using the affordability formulas lenders apply to mortgage approvals. Calculating how much house you can afford prevents falling in love with homes beyond your financial reach and ensures your house hunting focuses on properties within your price range.

The 28/36 Rule: What Lenders Actually Use

Lenders use the 28/36 rule to determine mortgage affordability:

- 28% Rule: Monthly housing payment ≤ 28% of gross monthly income

- 36% Rule: Total monthly debt ≤ 36% of gross monthly income

Real-World Example:

- Your monthly income: $6,000

- Max housing payment: $6,000 × 0.28 = $1,680/month

- Max total debt: $6,000 × 0.36 = $2,160/month

If you have existing debt:

- Car payment: $400/month

- Student loans: $100/month

- Total existing debt: $500/month

Your available housing budget:

$2,160 (max total debt) – $500 (existing debt) = $1,660/month for housing

4-Step Affordability Calculator

STEP 1: Calculate Monthly Housing Budget

Gross monthly income × 0.28 = Maximum housing payment

STEP 2: Subtract Taxes + Insurance

Maximum housing payment – Property taxes – Homeowner’s insurance = Mortgage payment

Estimates: $300/month taxes + $150/month insurance

STEP 3: Convert Payment to Loan Amount

At 7% interest, 30-year mortgage:

| Monthly Mortgage Payment | Loan Amount |

|---|---|

| $1,000 | $150,000 |

| $1,500 | $225,000 |

| $2,000 | $300,000 |

| $2,500 | $375,000 |

| $3,000 | $450,000 |

STEP 4: Add Your Down Payment

Loan amount + Down payment = Maximum home price

Complete Example:

- Income: $6,000/month

- Max payment: $1,680/month

- Minus taxes/insurance: $1,680 – $450 = $1,230 mortgage payment

- Loan amount at 7%: ~$185,000

- Down payment: $40,000

- Maximum home price: $225,000

Use these calculations as your starting point before house hunting. Knowing your real budget prevents wasted time viewing unaffordable properties and protects you from financial strain after purchase. For ongoing expense tracking during your home search, consider using budget planner templates to manage your down payment savings and closing costs.

Frequently Asked Questions

A checklist for home buyer planner is a structured evaluation form that helps prospective homebuyers assess properties during house hunting. It includes sections for property details, room condition ratings, exterior features, and home systems evaluation. Using the same format for every viewing creates consistent comparison data.

Typically, such a planner includes spaces to check the exterior, rooms, electrical, plumbing, kitchen quality, and other aspects of the houses. The buyer visually checks each of these while visiting the houses with the intention of later evaluating the houses objectively by comparison.

Application of an checklist for Home Buyer template will help to avoid any emotional decisions as well as any observation that may be left out during the process of buying a home.

It will help to have uniform evaluation criteria for all the properties that may be evaluated by individuals throughout the process. This will enable objective comparison of properties for individuals to make better decisions while avoiding emotions during the

Similarly, a consumer purchasing a home is provided with a venue to organize their activities by means of a structured checklist that they follow. If they do not have the checklist, they visit a few homes and then cannot clearly recollect certain information from the home they evaluated.

Before each viewing, remember to either print or load your checklist of home buyer planners. First, complete the details of property. Also, be sure to walk through the property systemically and mark ratings on each category.

Instead of filling out the checklist later based on memory, it is best done on-site so the details can be readily recollected later. Testing faucets, switches, and appliances can also be done on-site to have a better idea of their working abilities later on.

Once you have seen several properties, it would be best to compare all the completed checklists side by side so that the best choices can be determined. Organizing multiple viewings in one day works best when you use daily planner templates to schedule appointments and travel time between properties.

One complete checklist for a home buyer planner ought to have header fields for key property data. This is to say the address, listing price, square footage, number of bedrooms, number of bathrooms, year built, lot size, and taxes should be included.

The major parts should be the outside of the property and the inside of all rooms with condition scoring. There are also sections for home systems where you can check the electrical, plumbing, HVAC, and water heater.

Besides, kitchen assessment can cover cabinets, countertops, appliances, and layout. Also, note, taking is important to be able to record concerns, dimensions, or outstanding features that impact your decisions.

Yes, you can easily customize your checklist for the home buyer planner based on your priorities. Just add some space for the home office space, the size of the yard in relation to your pets’ sizes, etc.

Irrelevant sections may be removed, such as the basement evaluation for single-story homes. Additional factors may include the income generated or the renovation costs for investment properties. Personalization helps the planner meet individualized needs.

As you work through using a home buyer’s planner, consider expensive-to-repair home attributes that can dramatically affect home value.

These include foundation condition, roof lifespan, heating-and-cooling system functionality, and plumbing condition: these can range from $5,000 to 30+ thousand to replace.

Also, test the electrical capacity, look for water damage or mold, and inspect the appliances. Check the natural lighting, functionality of the layout, and enough available space. Never get too engrossed by the fixtures so that you overlook the important aspects.

Generally speaking, the majority of buyers are benefited by a minimum of two viewings, one for initial impressions and one for indepth inspections. Bring the prepared checklist to the second viewing to compare the initial ratings.

Alternatively, a third visit might be scheduled during a different time of day, particularly to ensure evaluation of the lighting, as well as the neighborhood itself. Competitive markets require quicker decisions while remaining rigorous with your evaluation.

This methodology must be employed every time, especially for objective evaluation. It might be worthwhile creating a separate notes planner templates for jotting down your meetings with real estate agents, mortgage agents, as well as home inspectors.

A home inspection checklist helps during initial viewings to spot obvious issues. It focuses on visible conditions you can assess during walkthroughs. This helps you decide which properties warrant serious consideration.

A professional home inspection occurs after your offer and provides detailed technical evaluation. It covers hidden systems, structural integrity, code compliance, and safety issues requiring expertise. Your planner screens properties initially; professional inspection validates your final choice.

A completed home buying checklist provides documented evidence of condition issues. When your checklist shows multiple problems, calculate repair costs and request price reductions. Systematic documentation demonstrates thorough evaluation rather than arbitrary demands.

Present your completed planner with condition ratings to your real estate agent. They can use this information to justify your offer price or repair requests. This objective, documented approach is more effective than vague concerns when negotiating.

You should change your home buyer planner checklist when you are looking at condos or townhouses. If it is a condo, concentrate on the features of the unit itself only like balconies instead of yards and roofing. Also, create sections for HOA fees, amenities, and the overall quality of building maintenance.

Add some questions regarding the degree of soundproofing, availability of an elevator, parking, and splitting of utility costs.

Also, get rid of the parts of the roof and exterior siding that were individually handled by the homeowner and managed to the HOA. Change the planner accordingly to different types of ownerships and various maintenance responsibilities.

The biggest mistake is focusing only on cosmetic features while ignoring structural issues. Other errors include skipping sections like basements, not testing systems, and rushing through properties. Many buyers fail to complete checklists on-site while details are fresh.

Buyers also forget to bring completed planners to second viewings for verification. Using inconsistent rating criteria makes comparisons difficult across properties. Always complete every section on-site, maintain consistent standards, and combine findings with professional inspection results.